Tan Song Cheng v PP

| Jurisdiction | Singapore |

| Judge | See Kee Oon J |

| Judgment Date | 09 June 2021 |

| Court | High Court (Singapore) |

| Docket Number | Magistrate's Appeals Nos 9758 and 9768 of 2020 |

[2021] SGHC 138

See Kee Oon J

Magistrate's Appeals Nos 9758 and 9768 of 2020

General Division of the High Court

Criminal Procedure and Sentencing — Sentencing — Appeals — Offenders pleading guilty to charges under s 96(1) Income Tax Act (Cap 134, 2008 Rev Ed) — Whether sentences manifestly excessive — Section 96(1) Income Tax Act (Cap 134, 2008 Rev Ed)

Criminal Procedure and Sentencing — Sentencing — Benchmark sentences — Offenders pleading guilty to charges under s 96(1) Income Tax Act (Cap 134, 2008 Rev Ed) — Whether available sentencing precedents laid down any sentencing benchmark or consistency in sentencing — Sentencing framework for offences punishable under s 96(1) Income Tax Act (Cap 134, 2008 Rev Ed) — Section 96(1) Income Tax Act (Cap 134, 2008 Rev Ed)

Revenue Law — Income taxation — Tax evasion — Failure to declare income consequent upon offenders' attempts to avoid goods and services tax — Sentencing considerations of offences of tax evasion

Held, dismissing both appeals:

(1) From the sentencing precedents for s 96(1) ITA offences, there had not been any consistent sentencing trend, despite the fact that such offences did not encompass a wide-ranging variety of circumstances. A sentencing framework would be appropriate as offences under s 96(1) of the ITA were not that factually diverse: at [28] and [29].

(2) The facts of Chng Gim Huat did not typify the usual circumstances of tax evasion, and the case did not appear to have provided a focal point for the comparison or calibration of sentences in subsequent cases. Accordingly, Chng Gim Huat did not lay down a benchmark sentence for s 96(1) ITA offences: at [32].

(3) Offences under s 96(1) of the ITA defrauded the State of its revenue. The primary mischief sought to be addressed by criminalisation of tax evasion under s 96(1) of the ITA was the failure of the offender to hand over what was due to the State, and the primary sentencing consideration should be that of general deterrence: at [34] to [36].

(4) Utilising a sentencing approach based on offence-specific and offender-specific factors, the list of factors provided in Logachev succinctly captured the various sentencing considerations relevant to s 96(1) ITA offences: at [37] and [38].

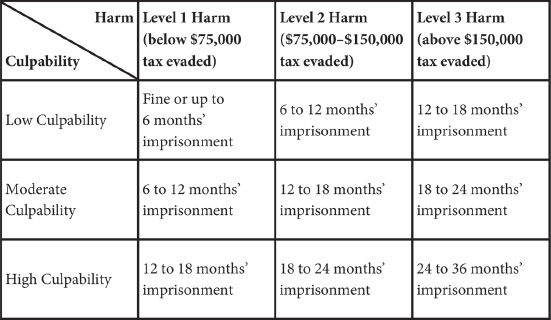

(5) Adopting the sentencing framework set out in Logachev, the first step was for the court to identify the fact-specific level of harm caused and the offender's culpability. The level of harm caused should be stratified into three levels of severity based on the quantum of tax evaded: (a) less than $75,000 (“Level 1 harm”); (b) $75,000–$150,000 (“Level 2 harm”); and (c) more than $150,000 (“Level 3 harm”). Having determined the harm based on the quantum of tax evaded, other factors such as the involvement of a syndicate or transnational element should be considered to adjust the severity of the harm caused: at [59] and [64] to [70].

(6) The imposition of the mandatory penalty of treble the amount of tax evaded should have little impact on the determination of the sentence, as the court had no discretion to determine it and it would be illogical that the greater the tax evaded and the greater the mandatory penalty, the less likely an offender would be subject to a more severe sentence or longer period of imprisonment: at [69].

(7) Having determined the level of harm caused and the offender's culpability, the second step would be to identify the applicable indicative sentencing range. Bearing in mind the sentencing range set out in s 96(1) of the ITA, and the stratified levels of harm identified, the following indicative sentencing ranges would be appropriate: at [71].

(8) Where appropriate, a non-custodial sentence could be considered, provided that any deterrent effect of a fine imposed would not be eclipsed by the imposition of the mandatory treble penalty: at [73].

(9) Having considered the indicative sentencing range, the third step was to identify the appropriate starting point within that range, having re-examined the offence-specific factors: at [74].

(10) The fourth step was for the court to make adjustments to the starting point based on the offender-specific aggravating and mitigating factors. At this stage, the total amount of tax evaded in both the proceeded charges and charges taken into consideration had to be considered: at [75] and [76].

(11) The fifth step was for the court to make adjustments to the sentence on account of the totality principle: at [77] and [78].

(12) In the First Appellant's case, the level of harm caused would fall within “Level 1 harm”. The First Appellant's culpability was low. Accordingly, a sentence of ten weeks' imprisonment was appropriate as a starting point, and having considered the First Appellant's offender-specific factors, the sentence of six weeks' imprisonment was appropriate. As the offences were committed in separate years of assessment, the one-transaction rule was not breached: at [80] to [85].

(13) In the Second Appellant's case, the level of harm would fall within “Level 2 harm”. The Second Appellant's culpability was low. Accordingly, the applicable indicative sentencing range lay between six to 12 months' imprisonment. In light of the absence of other harm factors and the fact that the amount of tax evaded lay just between “Level 1” and “Level 2” harm, a sentence of 16 weeks' imprisonment was appropriate as a starting point: at [87] to [90].

(14) The DJ had given due consideration to the Second Appellant's mitigating factors. Her personal circumstances did not create a dire and exceptional situation which compelled her to commit the offences. Having considered the Second Appellant's offender-specific factors, the sentence of ten weeks' imprisonment was appropriate: at [91] to [93].

Chang Kar Meng v PP [2017] 2 SLR 68 (refd)

Chng Gim Huat v PP [2000] 2 SLR(R) 360; [2000] 3 SLR 262 (distd)

Dinesh Singh Bhatia s/o Amarjeet Singh v PP [2005] 3 SLR(R) 1; [2005] 3 SLR 1 (refd)

Edwin s/o Suse Nathen v PP [2013] 4 SLR 1139 (refd)

Gan Chai Bee Anne v PP [2019] 4 SLR 838 (refd)

Huang Ying-Chun v PP [2019] 3 SLR 606 (refd)

Janardana Jayasankarr v PP [2016] 4 SLR 1288 (folld)

Lee Shing Chan v PP [2020] 4 SLR 1174 (refd)

Logachev Vladislav v PP [2018] 4 SLR 609 (folld)

Mohamed Shouffee bin Adam v PP [2014] 2 SLR 998 (refd)

Mohd Akebal s/o Ghulam Jilani v PP [2020] 1 SLR 266 (refd)

Ng Kean Meng Terence v PP [2017] 2 SLR 449 (refd)

PP v Chew Tiong Wei [2016] SGDC 59 (refd)

PP v Koh Thiam Huat [2017] 4 SLR 1099 (refd)

PP v Onn Ping Lan [2005] SGMC 8 (refd)

PP v Raveen Balakrishnan [2018] 5 SLR 799 (refd)

PP v Tan Fook Sum [1999] 1 SLR(R) 1022; [1999] 2 SLR 523 (refd)

PP v Tan Thian Earn [2016] 3 SLR 269 (refd)

PP v UI [2008] 4 SLR(R) 500; [2008] 4 SLR 500 (refd)

PP v Wong Chee Meng [2020] 5 SLR 807 (refd)

Suventher Shanmugam v PP [2017] 2 SLR 115 (folld)

Takaaki Masui v PP [2021] 4 SLR 160 (refd)

Tan Kiam Peng v PP [2008] 1 SLR(R) 1; [2008] 1 SLR 1 (refd)

Vasentha d/o Joseph v PP [2015] 5 SLR 122 (folld)

Wong Kai Chuen Philip v PP [1990] 2 SLR(R) 361; [1990] SLR 1011 (refd)

Yap Ah Lai v PP [2014] 3 SLR 180 (refd)

In unrelated proceedings before the same district judge (“DJ”), both appellants had pleaded guilty to charges of tax evasion under s 96(1)(b) of the Income Tax Act (Cap 134, 2008 Rev Ed) (“ITA”). Between 2008 and 2014, Tan Song Cheng (“the First Appellant”) as the director of TNT Cards & Silkscreen Pte Ltd (“TNTPL”) had permitted the reported sales revenue of TNTPL to be falsely reduced below $1m in order to avoid registering for goods and services tax (“GST”), which resulted in his employment income being reduced. Additionally, the First Appellant as the precedent partner of TNT Art & Silkscreen (“TAS”) had permitted TAS's reported net profit to be falsely reduced, reducing his share of TAS's trade income. Consequently, in 2009 and 2011, the First Appellant was undercharged $34,992.26 and $34,444.18 in income tax, respectively.

At the proceedings below, the First Appellant pleaded guilty to two proceeded charges under s 96(1)(b) ITA. Finding that there was no consistent sentencing trend in the precedents and that Chng Gim Huat v PP[2000] 2 SLR(R) 360 (“Chng Gim Huat”) did not set a sentencing benchmark, the DJ adopted the Prosecution's proposed five-step sentencing framework modelled on the sentencing framework set out in Logachev Vladislav v PP[2018] 4 SLR 609 (“Logachev”). Applying this framework, the harm and culpability of the First Appellant was found to fall in the low range. The DJ accordingly imposed a sentence of six weeks' imprisonment in respect of each proceeded charge, with both sentences ordered to run consecutively.

The First Appellant appealed against his sentence. He contended that the mandatory imposition of a financial penalty of treble the quantum of tax evaded would constitute sufficient deterrence, and that the amount of tax evaded should not be the primary metric for assessment of harm, and proposed an alternative sentencing framework. He also contended that the imposition of consecutive sentences offended the one-transaction rule.

Between 2009 and 2015, Lin Shaohua (“the Second Appellant”) as the precedent partner of Furniture Collection Centre (“FCC”) and Yang Hua Furniture Trading (“YHFT”), had permitted the reported sales figures for FCC and YHFT to be falsely reduced below $1m in order to avoid registering for GST. As a result, in 2016, the Second Appellant was undercharged $79.142.13 in income tax.

At the proceedings below, the Second Appellant pleaded guilty to one proceeded charge under the s 96(1)(b) ITA. The DJ similarly adopted the Prosecution's proposed five-step sentencing framework, and found that the Second Appellant's harm and culpability fell into the low range. The DJ accordingly imposed a sentence of ten weeks' imprisonment.

The Second Appellant appealed against her sentence. Similar to the...

To continue reading

Request your trial

-

Public Prosecutor v Hindakumbure Charindu Dilshan Rajapaksha

...behind why section 377BI of the Penal Code had to be enacted in the first place (Tan Song Cheng v Public Prosecutor and another appeal [2021] 5 SLR 789 (“Tan Song Cheng”) at [26]). In the present case, both the Prosecution and Defence did not – rightfully, in my view – request for a sentenc......

-

Public Prosecutor v Mu Shen and others

...was reaffirmed by High Court in PP v Law Aik Meng [2007] 2 SLR 814 (at [24]) and the recent case of Tan Song Cheng and Lin Shaohua v PP [2021] SGHC 138 (“Tan Song Cheng”) where See J stated at [72]: In this regard, I note that the Prosecution has argued that a fine should only be imposed in......

-

High Court Sets Out New Sentencing Framework For Tax Evasion Offences

...sentencing outcomes - is therefore crucial to ensuring a fair justice system. In Tan Song Cheng v Public Prosecutor and another appeal [2021] SGHC 138, the High Court agreed with the prosecution that previous sentencing decisions under section 96(1) of the Income Tax Act lacked a consistent......

-

Criminal Procedure, Evidence and Sentencing

...Masui [2022] 1 SLR 1033 at [15]. 105 Public Prosecutor v Takaaki Masui [2022] 1 SLR 1033 at [15]. 106 Tan Song Cheng v Public Prosecutor [2021] 5 SLR 789 at [65]. 107 [2021] 5 SLR 789. 108 Tan Song Cheng v Public Prosecutor [2021] 5 SLR 789 at [65]. 109 See para 15.20 above. 110 Cap 241, 19......

-

Revenue and Tax Law

...However, this rule is not inflexible; for example, an order mandating a tax refund was made in C v Comptroller of Income Tax.78 1 [2021] 5 SLR 789. 2 Tan Song Cheng v Public Prosecutor [2021] 5 SLR 789 at [5]. 3 Cap 134, 2008 Rev Ed. 4 Tan Song Cheng v Public Prosecutor [2021] 5 SLR 789 ......